Utility Sales Tax Exemption

WHAT IS A PREDOMINANT USE STUDY?

Predominant use studies go by many names. They're often referred to as utility studies or use analysis. Whatever name you know them by, predominant use studies can save your company thousands of dollars a year in taxes.

To perform a predominant use study, inspectors start by taking an inventory of all equipment and appliances serviced by the applicable utility meter. They note the location, function, and hours of operation of each item individually. They also record the cubic foot consumption measured by each natural gas meter and the kilowatt-hour consumption of each electric meter. In some states, these findings must also be certified by a registered engineer.

Next, the equipment is categorized as either exempt or non-exempt based on guidelines provided by the relevant state statute. For equipment that serves both exempt and non-exempt functions, specialists quantify the electricity and/or natural gas used for each function.

If a utility meter is used predominantly for exempt functions, some states waive the sales tax for all of the energy consumed through that meter. In other states, only the portion of energy used specifically for exempt functions qualifies for the sales tax exemption.

OUR PROCESS

1. Complimentary Review

We analyze a client's utility invoices for each location to assess eligibility and determine the probable savings from the exemption. Upon completion of this review, a feasibility analysis is prepared and given to the client.

2. Utility Study

Specialists perform a detailed analysis of the client's utility usage at each location. In doing so, they determine the percentage of utility that qualifies for sales tax exemption.

3. Refund Filing

B. Riley submits a request for a refund of sales tax to the state for review and approval. Our experts communicate directly with the state to answer questions. Through this line of communication, we also ensure the client is fully refunded for all sales tax due.

4. Approval

Upon state approval, the client receives a lump-sum tax refund in the form of a check or credit to their utility accounts. We also file an exemption certificate for each utility account. This prevents the client from future sales tax charges on the exempt portion of their usage.

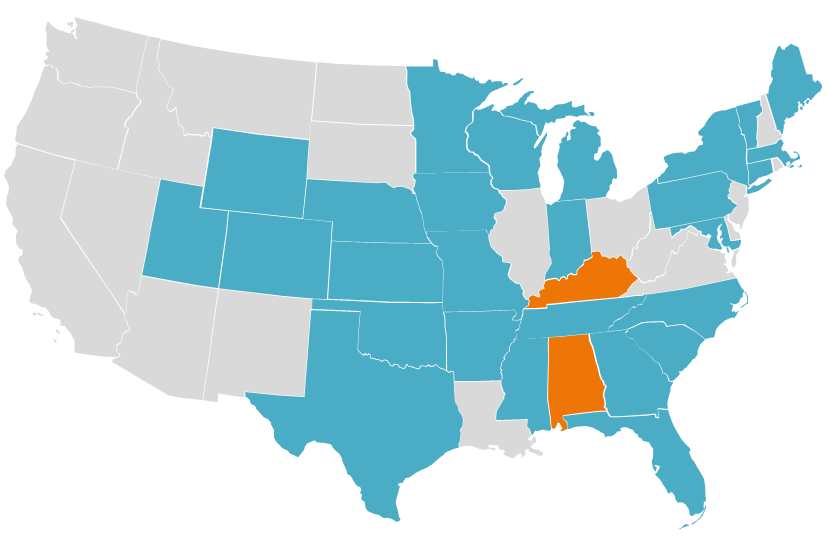

STATES OFFERING UTILITY SALES TAX EXEMPTIONS

Exemption statutes are significantly different from state to state regarding the taxability of certain utility usage. Additionally, each state is unique in the documentation it requires to support the exemption claim. Limited exemption offering for Kentucky and Alabama.

INDUSTRIES THAT QUALIFY FOR UTILITY SALES TAX EXEMPTIONS

Utility sales tax exemptions primarily provide tax relief for manufacturing companies. However, manufacturing can take many forms and is not limited merely to manufacturers producing retail products. Industries that could benefit from a predominant use study include:

Agriculture

Assisted Living Facilities

Data Centers

Fabrication

Food Processing

Hotels

Housing Complexes

Manufacturing

Mining

Oil Extraction

Processing

Recycling

Refineries

WHEN SHOULD YOU COMMISSION A PREDOMINANT USE STUDY?

If your company has never commissioned a predominant use study, the sooner you do so the more you'll save. Electricity, natural gas, and water used by qualifying equipment will be exempt from sales taxes moving forward. And many states will even issue refunds for these taxes dating back as far as 48 months.

In most states, the findings of a predominant use study grant tax exemption until there is a "significant change" in your business's operations. However, some states require a new study every three years. We will advise you on your state's requirements and recommend follow-up studies when necessary to ensure that your company maintains its tax exemption.

It's also important to commission a new study during or before:

- Mergers/Acquisitions

- Opening A New Location

- Signing With New Utility Vendors

SPECIALIZED EXPERTISE TO HELP YOU CAPITALIZE

B. Riley has the specialized expertise needed to help eligible clients capitalize on the utility sales tax exemption. Our utility tax specialists manage the entire exemption process for each client, from qualification to refund. Additionally, our tax attorneys and engineers review each utility study and exemption claim to ensure compliance and accuracy.

In many cases B. Riley works on a contingency-fee-basis, meaning the client owes nothing until savings are achieved through the exemption. Unique savings opportunities such as the utility sales tax exemption call for trusted experts with specialized experience. B. Riley has the expertise needed to diligently represent clients and achieve optimal savings through the exemption.

In addition to performing predominant use studies, we offer a variety of financial valuation services to find savings for our clients. Reach out to us to learn more about the various ways that we can save your company money.

ELIGIBLE STATES

Taxpayers with manufacturing or processing facilities located in the states below are eligible for the utility sales tax exemption.

KEY CONTACT

Kennedy White

Director